Starting a security guard company in California is a big step—and an exciting one. But with the responsibilities of protecting people and property comes a crucial legal and business requirement: General Liability Insurance. If you’re new to this industry, understanding your policy and what’s listed on your Certificate of Insurance (COI) is not just helpful—it’s essential. In this guide, we’ll break down the basics of your general liability policy, explain the meaning behind those confusing numbers on your COI, and highlight why maintaining this coverage is key to keeping your BSIS PPO license in good standing.

What Is General Liability Insurance?

General Liability Insurance (GLI) protects your security company from third-party claims involving:

- Bodily Injury (e.g., someone gets hurt on your job site)

- Property Damage (e.g., damage caused by a guard)

- Personal and Advertising Injury (e.g., claims of slander, libel, or false arrest)

This policy is required by California law if you’re operating under a PPO (Private Patrol Operator) license, regulated by the Bureau of Security and Investigative Services (BSIS).

Why Is It Required by BSIS?

The BSIS mandates general liability coverage to ensure security companies are financially able to handle claims or lawsuits if something goes wrong on the job. It protects:

- The public

- Your clients

- Your business

- Your license

If you let your policy lapse—even by accident—you risk suspension or revocation of your PPO license.

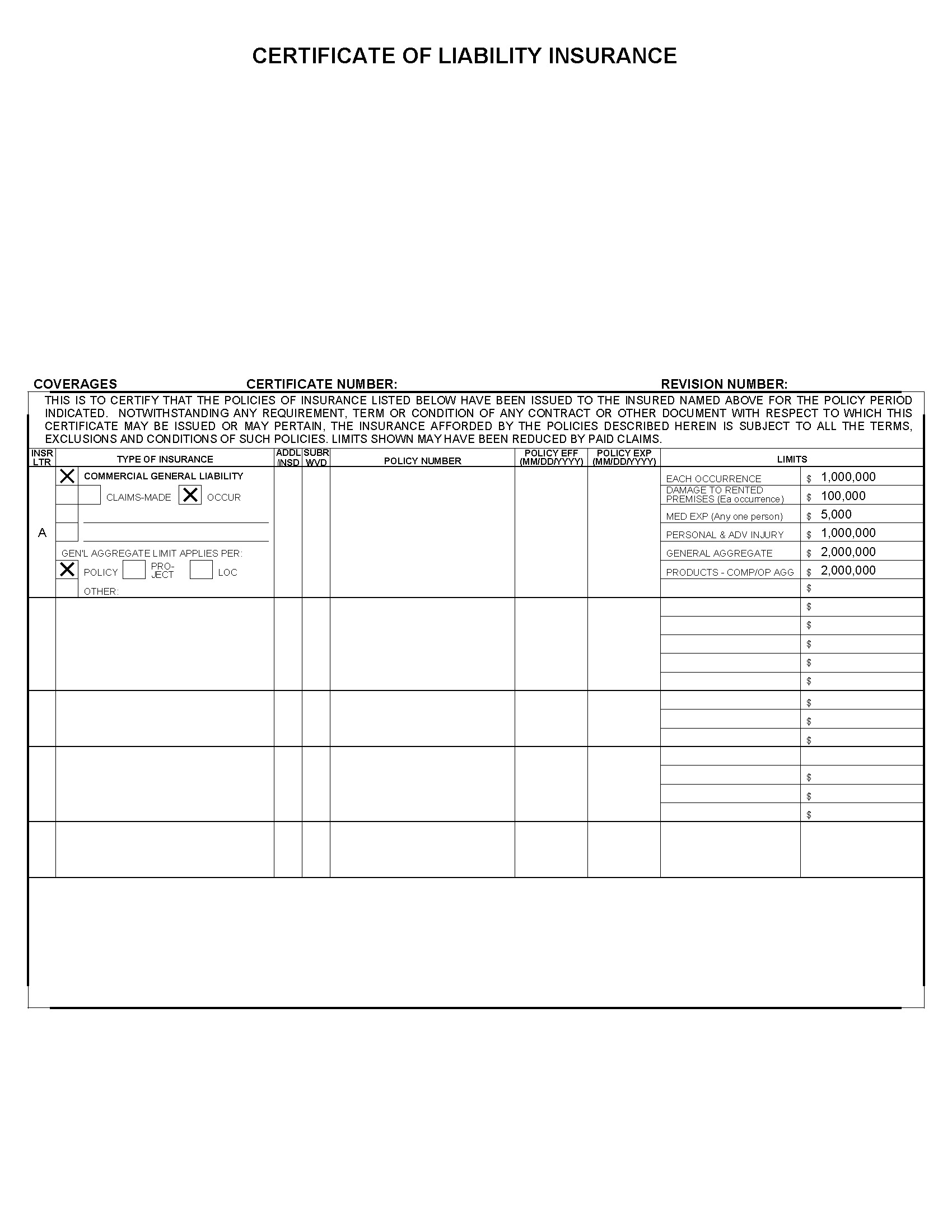

Understanding the Certificate of Insurance (COI)

Your COI is a one-page summary of your insurance coverage. It’s what you’ll often provide to:

- Clients requesting proof of insurance

- The BSIS for license renewals

- Vendors or property managers before starting a contract

Let’s break down the key parts of the COI:

1. General Aggregate Limit

This is the maximum amount your policy will pay for all claims during your policy period (usually 1 year).

👉 Example: $2,000,000

2. Each Occurrence Limit

This is the maximum amount paid per individual claim for bodily injury or property damage.

👉 Example: $1,000,000

3. Personal & Advertising Injury Limit

Coverage for non-physical claims like slander, libel, false arrest, or invasion of privacy.

👉 Example: $1,000,000

4. Damage to Rented Premises

If you damage a property you’re renting (like an office), this is the max your insurer will pay.

👉 Example: $100,000

5. Medical Expense

Pays for minor medical claims without needing to determine fault.

👉 Example: $5,000

6. Policy Effective and Expiration Dates

Make sure these dates never lapse. Your coverage must remain active to stay in compliance with BSIS requirements.

Minimum Coverage Requirements for PPO License (as of latest BSIS rules)

- Minimum $1,000,000 per occurrence for each occurrence for initial licensure

- Have the required insurance in effect at the time of license renewal and for the continued maintenance of the license. (Business and Professions Code Sections 7583.39 and 7583.40)

Check with BSIS or your insurance broker to confirm the latest minimums, as regulations may update.

Why Keeping This Coverage Active Matters

Failing to maintain your general liability insurance can result in:

- Immediate suspension of your PPO license

- Ineligibility for renewals

- Loss of contracts or clients

- Exposure to legal liability without protection

If your policy cancels, lapses, or is non-renewed, your insurance provider is required to notify the BSIS.

Tips for Staying in Compliance

- Set calendar reminders for renewal deadlines.

- Work with an insurance agent experienced with security industry policies.

- Review your COI annually to confirm correct limits and active coverage.

- Notify your insurer of changes, such as expanding services or new locations.

Final Thoughts

Your General Liability Insurance policy isn’t just a checkbox—it’s your company’s financial safety net and your license lifeline. By understanding the details of your coverage and keeping it active, you’re not only protecting your business—you’re also staying compliant with California’s BSIS regulations.

Need help reviewing your current policy or finding the right coverage? Work with a broker who understands the unique needs of security guard companies in California.